Choosing the right core banking platform

Core banking systems can easily be considered the boring bit of banking, yet it is the core system that has the power to enable – or constrain – the growth of any organisation offering financial products. Core banking technology is at the centre of everything, ledgers, data, connectivity to the wider provider ecosystem – it all resides within the core. Choosing the right core to deliver innovation both now and in the future is the first step to building or reinvigorating a successful financial offering. From the smallest challenger to the biggest financial institution, the choice of core can make or break the business.

The Challenges

New Entrants

For new entrants to the market, the choice of a core system will set the scene for everything going forward. They need a core that will ease the process of building a unique ecosystem to deliver new products and services. They count timelines in days not months so they need to get to market fast. For start-ups, budgets are often tight, so every delay prior to launch hurts. They need a cost-effective core banking system that can move fast, flex as things change and work seamlessly with a wider eco-system through the use of open APIs. When opportunities arise the core must also provide the ability to pivot to offer new products and services without the need to purchase new product modules with all the costs and time implications they bring.

Incumbent banks

Whilst new entrants are hitting the market with innovative products and new ways of banking, there are banks steeped with tradition and history who, despite their deep pockets, are struggling to keep up. Historically, people used to stick with a bank for life, but that is no longer the case. Most people bank with more than one bank and it is the bank with the best technology to drive great customer experiences that will emerge victorious. Unfortunately, the same legacy that can lend the perception of stability and gravitas to a bank, usually also means outdated legacy technology. Banks built over decades or longer are often underpinned by a maze of old systems that simply weren’t designed for speed, flexibility or connectivity in today’s ‘instant’ world. The risk of making a wholesale change to a new core can be daunting – but the opportunity risk of not doing so is even greater in the long term. The challenge is delivering products and services to compete with the challengers without compromising the stability of their existing business.

Finding a solution

New Entrants

For new entrants, the path is clear to choose the most cost-effective route to get to market fast by choosing NextGen cloud-enabled core banking that can scale as the business grows. Choosing a core tech provider who will work in partnership, with flexible charging, a good understanding of the challenges facing new entrants and using agile methodology helps new entrants get to market fast with as little red tape as possible.

Whilst the temptation may be to choose an off-the-shelf BaaS solution, ultimately this approach stifles innovation, restricts capabilities and stunts growth. If everyone is locked into the same tech stack how can they create something special and keep ahead of the market? For those aiming to build innovative solutions and lead the market, building an ecosystem of best-of-breed partners can be best delivered by a SaaS core banking platform. Open APIs can deliver a world of opportunities for innovation through unlimited partner relationships.

Incumbent banks

For legacy banks, the choice is more complicated. Whilst they want all the features expected by a challenger, they also need to ensure that the new core can drive innovation without toppling the delicate balance of the existing systems. This is where the co-existence model comes into play. A NextGen core can run in parallel with the existing tech to drive innovation for new product releases, without impacting the existing customer experience. This affords the bank the opportunity to innovate without having to wait for a risky big bang migration.

We’ve all seen the disastrous outcomes of big bang migrations such as the experience of Lloyds TSB in 2018 where customers were locked out of their accounts for up to 5 days, found money was missing and could see the accounts of others.

With a co-existence model using a cloud-based core, this risk can be mitigated. Data migration can run in parallel with the old systems, going through rigorous testing well before flicking the switch to make the new technology live for customers.

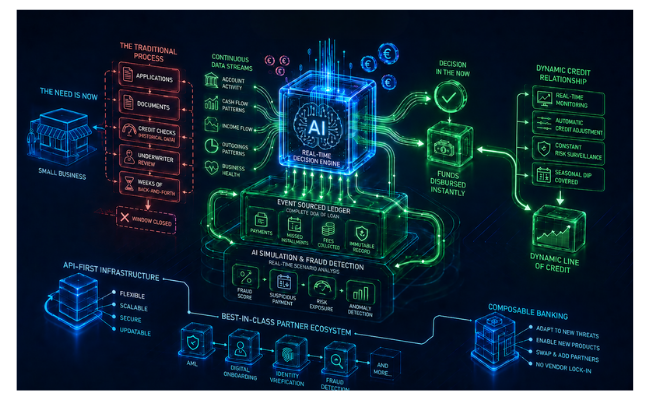

Future-proofing with a flexible ecosystem

True innovators know that today’s exciting new product feature can be tomorrow’s hygiene factor, so it is important to build any financial services offering on a stable foundation that will enable ongoing change swiftly and without huge overheads – financial, technical or human. Choosing a data-driven SaaS core banking solution makes it possible to build innovative, tailored and scalable product and service offerings that will flex with customer demand, changing economic conditions, regulatory updates or advances in technology.

Open APIs allow partnering with a wide range of providers and changing to new ones when required. A key to making the most of this flexibility is real-time data. Open APIs will deliver little in terms of customer experience without the real-time data to drive exceptional customer experience, whether that be for onboarding through biometric verification or delivery of push notifications when making transactions.

Even relatively young financial institutions have found themselves stifled by legacy systems within a few short years, either by choosing pre-packaged solutions or choosing first-generation cloud technology that has long since been surpassed. To avoid this happening it is essential to choose a core that uses the very latest cloud-native architecture, powers product diversification and enables unlimited partner integrations.

Efficient Implementation

So once requirements have been gathered, analysed and documented, the project set up, and effort estimated – either with a consultant or an internal team – the choice of technologies will finally be made. Unfortunately, this is where the project can lose momentum. Many companies will simply not have the resources and experience to run a large-scale project without impacting BAU. This is where an experienced systems integrator will make all the difference. They can apply proven project methodology, use their deep technical knowledge of the core system and leverage their experience working with a range of partners to streamline the process of implementing the ecosystem to deliver the business vision.

For existing businesses with live customers, all this can be done in a co-existence model, making it possible to run an innovation project in parallel to existing business without service degradation. An experienced systems integrator will leverage the knowledge of the existing business teams to streamline the process whilst still enabling them to continue with their day jobs. Taking this approach ensures that existing customer service levels can continue uninterrupted while development work continues to deliver innovation. Better yet, before implementing the full migration, the bank can choose to onboard new customers straight to the new system whilst completing the migration in designated tranches for full control and risk mitigation. Choosing the right partner is key to success in this endeavour. A system integrator must combine a strong technical skill set with a comprehensive knowledge of the business. Furthermore, to streamline this process and to avoid unnecessary handovers, it is key that the specialist you are working with can carry the project through the entire lifecycle, from design and analysis to implementation and testing and onto deployment and production support. Make sure you can embrace the change with confidence by not only selecting the right product but also the right integration partner.