To unleash the power of next-generation fintech, FIs must adopt next-generation operational models.

Successful businesses know that success relies on putting the customer at the centre of everything they do, but sometimes this aim gets lost in the day-to-day running of the business. Over time, silos develop between departments, or even within departments, and suddenly understanding of the end-to-end customer journey becomes fragmented. Much of this opacity comes from disjointed legacy systems – each holding a bit of the puzzle but never connecting to form a complete picture.

No company wants to be mired down in a web of legacy systems – given the choice most leadership teams would opt for new technology to allow them to reduce overheads, improve customer experience – and importantly – keep up with the competition. But the risk of migration is incredibly intimidating. Nobody wants to put their head above the parapet in a board meeting to propose moving the business lock, stock and barrel to a new technology provider. We’ve all seen it go horribly wrong, so often the choice to modernise will be left until disaster strikes, or when systems can no longer cope with business volumes or regulatory demands.

Modernising isn’t just about technology

As they say in self-help groups – first you need to admit you have a problem. Unfortunately, even when admitting there is a problem, sometimes the solution is focused purely on the tech and not on the operating model. Where siloed working practices have existed over extended periods of time it can be hard to stand back and look at the big picture. To make the most of next-generation technology to achieve great results for your customers and your business, you must also take a hard look at the operating model. That means changing the way the team works together to refocus on the customer. From development through to delivery, having teams from all areas of the business work together to build the customer journey allows the technology and the customer services teams to bring a wide range of expertise together to create customer experiences that take the entire journey into account. Removing developers from the customer experience and the operational product owners from the development process results in fragmented, interpreted requirements rather than allowing an ongoing dialogue and testing which is the hallmark of agile development.

Using technology to trigger operational change

In many ways, legacy systems can make it difficult to adopt next-generation operational models as each product may sit on different technology creating functional barriers. By implementing next-generation core banking technology it is possible to start tearing down the barriers – but operational behaviours need to take that journey too. Of course, every customer journey will traverse a number of technologies to deliver different experiences such as KYC and digital front end, but with those technologies aligned at the core, the process of bringing it all together into a seamless customer experience can begin.

Taking control and reducing risk

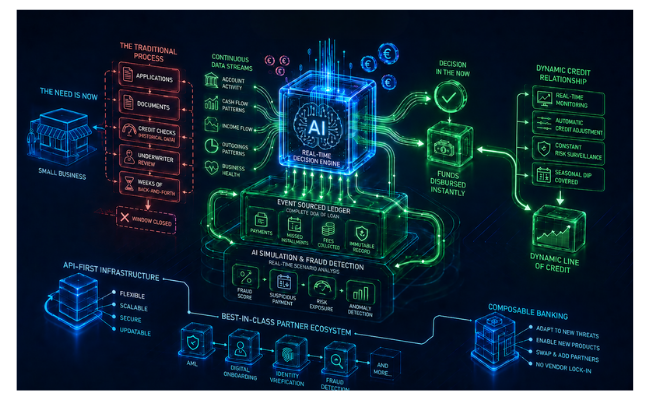

Implementing a next-generation multi-product banking core will power fast product innovation but equally important is the flexibility it will afford in allowing controlled migration of legacy products. In fact, adopting a next-generation banking core will enable legacy systems to be shadowed to ensure that data flow can start well before products are moved onto the new system. So whilst the new core is being used to build new innovations, it can also be used to start a controlled migration of legacy business. Indeed, existing products can be rebuilt on the new system with all the same features (and quite likely some shiny new ones) allowing new customers to be onboarded through the new technology either before or in conjunction with controlled migration from the legacy system. For risk teams, this gives the opportunity to see the new core in action well before the entire customer book is migrated.

Ecosystem

With legacy systems there will often be a number of product-centric ecosystems in play. Each working in parallel internally but being experienced across products by customers. Whilst there will clearly be different technologies required for different products such as loan origination or card services, breaking down the product silos will make it possible for customers to go through a consistent onboarding and servicing journey across all products – giving them a seamless brand experience. To make this happen both the tech and the operational team need to go on a journey to change the way products and services are delivered.

Reaping the benefits of NextGen

Tearing down product silos and aligning cross-functional teams will undoubtedly bring benefits to both the customers and the business, but by choosing a NextGen data-driven core the business will also benefit from improved customer insights and reporting capabilities across the entire business. This means that the business will be prepared for anything the regulator or market conditions might throw at it. When that dreaded ‘Dear CEO’ letter arrives from the FCA, having access to a full history of all transactional records and interactions across all products simplifies the process of creating bespoke reporting for specific requests. When market conditions change and you need to understand your customers in new ways, the data is there – across all products. And if you’ve chosen a NextGen core banking platform like SaaScada, the business unit also has the ability to action the data-driven decisions quickly without the need for huge developer overheads.

Taking it slow or taking the plunge

Making the decision to adopt NextGen technology is the first step towards modernising a financial offering but to release the power of NextGen core technology, the culture of the business has to go on that journey too. But that can take time. The beauty of a cloud-native data-driven platform is that it can operate in concert with legacy systems and offer the ability to move at a pace that minimises risk whilst still delivering rewards. If you would like to know more about how we can help you take the next step please contact us.