Who’s Ready for Agentic AI in Banking?

Executive Summary

Agentic AI is quickly moving from concept to reality. Across industries, organisations are exploring and implementing autonomous systems to make decisions, optimise processes and reshape how services are delivered. Agentic AI in banking, however, is struggling to get beyond exploration.

While there is no shortage of ambition, most banks are still constrained by the legacy systems, fragmented data and manual processes that sit at the heart of their operations. As a result, there is a growing disconnect between what banks believe AI can deliver and what they can execute today.

Our survey of 150 banking innovation leaders highlights a blunt reality:

- Banks overwhelmingly believe agentic AI will transform their industry.

- But very few are operationally ready to take advantage of it.

- And many are still struggling with the same core challenges they have faced for years.

The result is a widening gap between AI ambition and operational reality. Banks that fail to bridge this gap risk being left behind. Not because they lack vision, but because their foundations cannot support it.

“Trying to build AI on ancient legacy foundations is like racing an Aston Martin over cobblestones: it’s going to be a bumpy ride. If banks are serious about getting ahead with AI, they need data and core systems that are fit for purpose.”

– Steve Round, Co-Founder and President, SaaScada.

Key findings:

- 91% think agentic AI will enable entirely new ways of designing banking services and making decisions.

- Only 1-in-10 banks have largely automated processes like standing orders and payments.

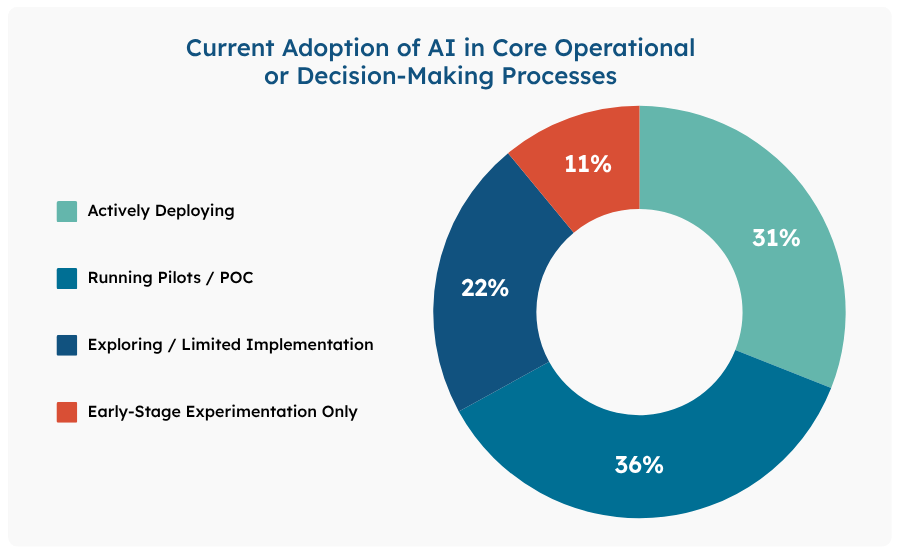

- Less than a third are actively deploying AI in core operational or decision-making processes.

- 77% say their ability to adopt AI is significantly impacted by legacy systems restricting data availability.

- Only 12% are very confident that their organisation could clearly explain and justify AI-driven decisions to regulators today.

Agentic AI – the Next Frontier of Banking?

There is no doubt that the potential for agentic AI use cases in banking is capturing the attention of innovation leaders:

- 83% think it represents one of the few genuinely transformative opportunities for banks to improve efficiency and remain competitive.

- 91% think it will enable entirely new ways of designing banking services and making decisions.

- 90% think it will deliver meaningful operational gains across core banking functions (such as reconciliation, payments monitoring, risk analysis and credit assessment).

From compliance to payments and risk, banks see significant potential. But while most think agentic AI in banking will deliver meaningful operational gains, their ambition remains limited. High-visibility use cases, like AI compliance monitoring and payments, are being prioritised above more fundamental operational processes.

Agentic AI’s Biggest Operational Potential

- 57% – Compliance monitoring and reporting.

- 51% – Reconciliation and exception handling.

- 46% – Payments monitoring and investigation.

- 42% – Risk analysis and credit assessment.

- 37% – Customer servicing and account administration.

- 34% – End-of-day/overnight operational processes.

However, the data shows many banks are still in the starting blocks when it comes to AI – let alone getting to the stage where they may be able to apply agentic technologies.

Just 31% of banks are actively deploying any type of AI in core operational or decision-making processes – with most still stuck in the exploratory or proof of concept stages.

“Agentic AI offers an entirely new way of working and tackling problems: the potential to reimagine banking processes is immense. We are already seeing fully agentic banks coming to market who will be able to launch new products and pivot service offerings at a lightning pace. Yet, while there’s no shortage of AI pilots in banking, the big challenge is turning those into real, scalable outcomes.”

– Nelson Wootton, CEO and Co-Founder, SaaScada.

Manual Processes vs Automation: A Clear Divide

The desire to harness agentic AI use cases in banking is at sharp odds with the reality most banks are living with day-to-day – where many of the processes that keep them running are still manual, time-consuming and prone to error.

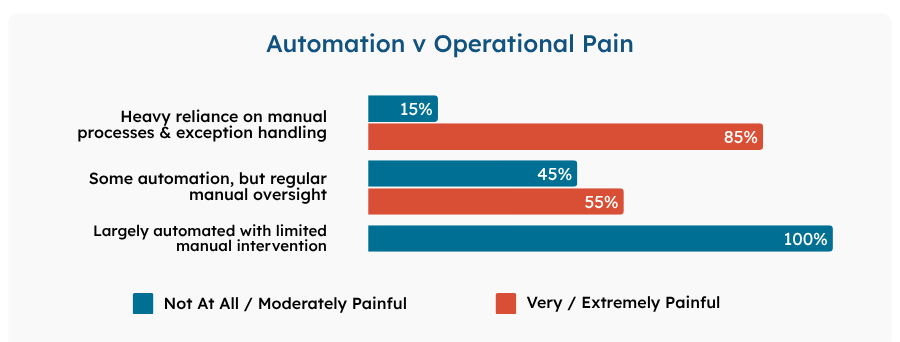

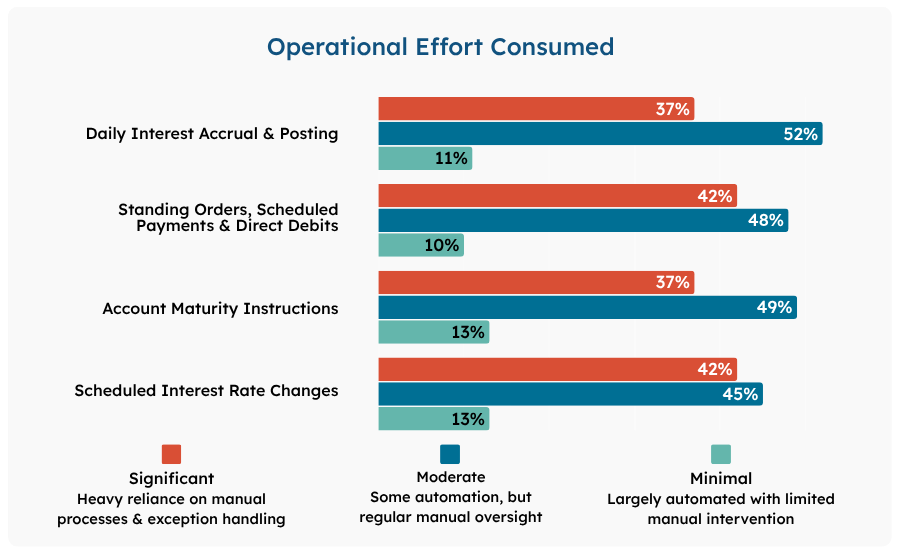

Take, as an example, the critical process of calculating and applying daily interest. Each day, across millions of accounts, banks must calculate accruals, reconcile data and apply postings. This is a huge lift for banks:

- 89% say this process is painful in terms of cost, manual effort and risk.

- 63% describe it as very or extremely painful.

The same pattern emerges across standing order and scheduled payments, account maturity instructions and interest changes.

When looking at what makes these processes so difficult, a clear correlation emerges:

- Banks that rely heavily on manual processes report higher levels of pain

- Those that are largely automated report little to no pain across all functions

Despite ongoing struggles, automation remains the exception, not the rule. For example, only 1 in 10 banks have largely automated processes like standing orders and payments.

“Banks can’t expect to innovate with agentic AI if they are still mired in manual processes. The priority has to be maturing the infrastructure and driving automation first. Only then can banks layer in AI and start to see real operational gains.”

– Paul Payne, Chief Technology Officer, SaaScada.

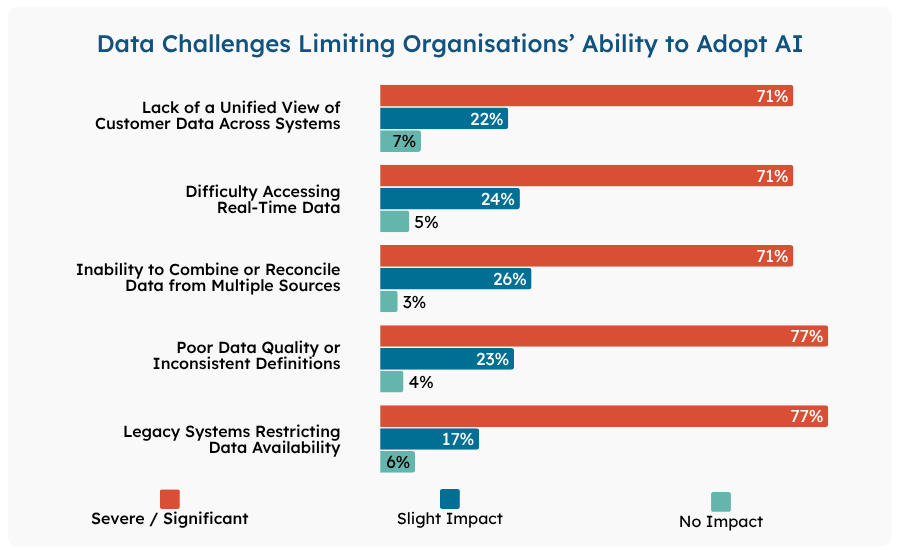

Data Barriers to Progress

Beyond a lack of automation, data challenges are a core barrier to banks achieving their AI ambitions.

It isn’t just data access that’s the challenge. Regulation and poor data quality are emerging as critical barriers. If banks can’t trust the data feeding these models – or explain the outcomes – both institutions and customers are put at risk.

- Stuck between a rock and a hard place: 80% think banks are caught between moving too slowly on AI and falling behind competitors or moving too quickly and being exposed to regulators.

- Poor data quality risks harming the most vulnerable: 72% warn that poor data, inherited bias and insufficient oversight will leave banks dangerously exposed as AI adoption accelerates. Meanwhile, 79% believe that without high-quality, explainable data, AI could worsen financial exclusion, rather than improving it.

- Transparency is essential but largely out of reach: 87% say to succeed with AI, banks must balance efficiency gains with explainability, resilience and trust. Yet only 12% are very confident their organisation could clearly explain and justify AI-driven decisions (e.g. credit, risk or customer treatment) to regulators today.

“Banks are facing pressure from all sides, as they are pushed to adopt AI while also proving that it’s fair, explainable and accountable. Without clean, accessible, real-time data, AI simply can’t deliver on its promise. AI is only as good as the data behind it – and right now, many banks don’t have the basics in place to support it.”

– Steve Round, Co-Founder and President, SaaScada.

From Ambition to Execution

The message is clear: the opportunity presented by agentic AI in banking and its potential to transform operations, decision-making and customer experience is understood. But most banks are not ready.

Legacy systems, fragmented data and manual processes are creating a drag on progress – slowing adoption and limiting impact.

To move forward, banks need to rethink their foundations.

SaaScada’s cloud-native core banking platform can operate as a primary core, or run alongside an existing legacy core system, to address exactly these challenges – enabling:

- Real-time data access.

- Fully automated processing.

- Scalable, flexible infrastructure.

By removing the operational constraints of legacy systems, banks can:

- Modernise incrementally.

- Unlock the value of AI.

- And move from experimentation to execution.

“Ultimately, agentic AI will reshape banking. But it won’t succeed without change at the core, which doesn’t happen overnight – although nowadays it is possible within a matter of months. The banks that succeed with AI won’t be the ones with the best ideas, they’ll be the ones with the right foundations to deliver them.”

– Nelson Wootton, Co-Founder and CEO, SaaScada.

Methodology

The data was gathered in March 2026 from 150 UK-based business heads/C-Suite staff at retail and business banks who are responsible for product innovation (e.g. Heads of Digital Transformation/CTOs/Chief Innovation Officers/Heads of Innovation/CEO). The banks had a balance sheet size of £0.5Bn – £100Bn.