Savings Accounts: AI That Makes Your Money Work Harder

The savings account has a problem. It sits there, waiting. It does not know that the balance could be earning better interest in a different account. It does not know when you could afford to put something aside. It certainly does not know that you have a holiday in six months and have not started saving yet. It just waits, passively accumulating whatever the customer remembers to deposit.

That model is about to be disrupted.

AI-driven savings do not wait. But a savings account cannot build this picture on its own, it only sees money arriving and leaving. The intelligence comes from elsewhere: a linked current account held at the same bank, or open banking connections to accounts held at other institutions. Either way, the AI gains a view of income patterns, spending rhythms, and existing commitments. When monthly pay is deposited and the data shows the balance comfortably above the customer’s typical spending needs, it automatically sweeps the surplus into a higher-yield savings pot. When the spending picture suggests a large bill cycle is approaching, it refrains from sweeping, protecting liquidity. When a goal deadline is approaching and the target is off track, it adjusts the automatic contribution upward. This is not a smart notification, it is financial behaviour that happens without the customer having to think about it.

The intelligence does not live in the savings account itself, it lives in the connected data picture. A linked current account or open banking feeds are what give AI the context to act at the right moment.

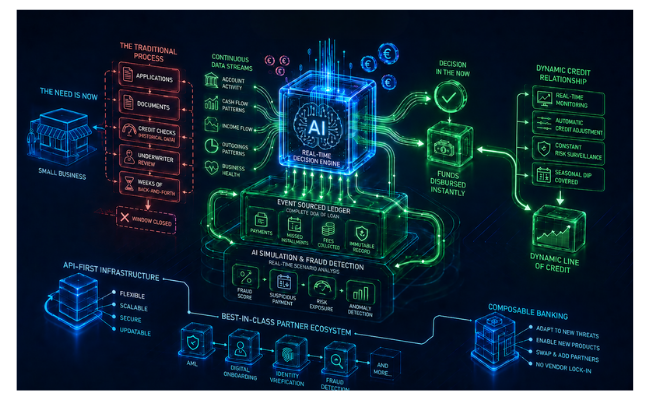

The real breakthrough is predictive wealth management. This is only possible on a core banking platform built to deliver real-time data, not one that assembles information hours after the fact. Where a customer holds their current account at the same bank, SaaScada’s real-time event stream gives the AI a live, granular view of spending behaviour, allowing it to predict when surplus cash will be available before it accumulates. Where the transactional relationship sits elsewhere, open banking APIs deliver the same picture. Either route, the AI acts at precisely the right moment, executing micro-savings into higher-interest pots when the customer can genuinely afford it, without risking liquidity later in the month.

This kind of banking automation software removes the cognitive burden from the customer entirely. Rather than a tool that prompts and reminds, it becomes a system that acts on the customer’s behalf, within boundaries they have defined, continuously optimising their financial position without requiring their attention.

API-first infrastructure extends the picture further still. A savings platform connected to investment platforms, pension providers, and goal-based financial planning tools builds a comprehensive view of the customer’s entire financial life, one the AI can act on intelligently. This composable banking approach means that as new technologies emerge, those partners can be integrated for the benefit of customers, without disrupting existing infrastructure, ensuring the platform evolves with the market.

Hyper-personalisation in savings is not about offering a slightly better interest rate to a broad segment. It is about learning from an individual’s patterns, knowing that it is likely the customer has a tax bill due in February, a holiday planned for September, and a pattern of overspending in December, and configuring their savings product automatically to navigate all three. That knowledge comes from connected data. Real-time APIs, open banking, and multi-ledger product configurability make it possible.