Lending in the Age of AI: Decisions Made in the Now

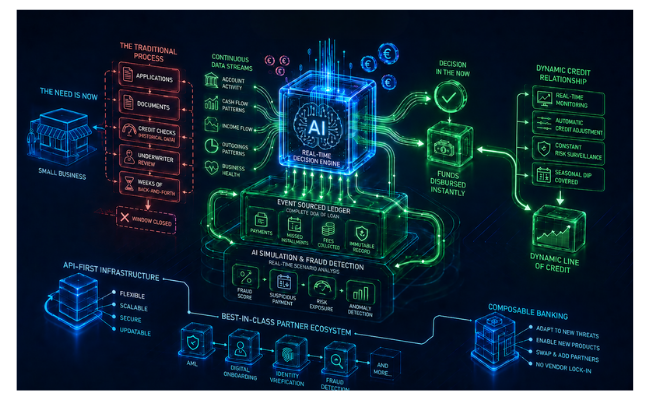

There is a moment every small business owner knows well. The moment they realise they need funding. Maybe a large contract has landed and they need to move fast. Maybe a supplier is offering a discount for early payment. Maybe cash flow is tight and payroll is three weeks away. In each case, the need is immediate. The traditional response is not.

Applications. Documents. Credit checks drawn from historical data. Underwriters reviewing files. Weeks of back-and-forth before a decision arrives, and by then, the window has often closed.

AI is not just accelerating that process. It is replacing it with something fundamentally different: cash-flow based lending.

The decision does not happen at the end of an application process. It is forming continuously, based on data the bank already holds, enriched by a connected partner ecosystem.

A modern digital lending platform does not wait for an application detailing a snapshot of financial history, AI-driven lending uses continuous, real-time observation of financial behaviour. How does income flow through this account? How does the customer manage irregular months? What does the pattern of outgoings reveal about business health? These signals, drawn from live transaction data and a full event history, not static bureau files, give a richer, more honest picture of creditworthiness than any traditional score.

Architecturally, Event Sourcing transforms what is possible in loan servicing software. The ledger maintains a complete event history of every loan: every payment, every missed instalment, every fee accrual, all captured as an immutable record. AI can run simulations on this data to see how a rate change or a missed payment would affect total risk exposure in real time. Before deploying a new repayment structure or a modified interest tier, banks and alternative lenders can model the impact across real customer profiles, giving both institution and customer complete clarity before any change goes live. Legacy loan servicing software has never been able to offer this level of dynamic simulation, because it was built to record, not to reason.

This also unlocks a fundamentally different kind of credit relationship. Rather than a fixed facility reviewed annually, banking automation software powered by AI can monitor a small business’s real-time transactional ledger and automatically extend a line of credit during a seasonal dip, de-risking the loan through constant, automated surveillance rather than periodic manual reviews. The credit facility becomes dynamic, adjusting to the customer’s actual financial reality as it evolves. This is what separates a genuine digital lending platform from a traditional system with a digital front end.

API-first infrastructure ensures that best-in-class partners, for AML, digital onboarding, identity verification, can be integrated without rebuilding the core, and updated as the ecosystem evolves. The composable banking model means that as new threats emerge or new products are required, the partner network adapts without the institution being locked into a single vendor’s roadmap.

Lending is not slow by necessity. It is slow because most systems were built for a world where humans had to gather information, analyse it, and decide. In a world where AI does all three, continuously, from live data, the traditional wait for approval becomes a relic of a different era.