Transactional Accounts: The Banking Nerve Centre

The transactional account has been the foundation of retail banking for generations. It is where wages land, bills leave, and the financial life of a customer plays out in real time. For most banks, it has also been the product most taken for granted, a transaction container, quietly processing debits and credits, rarely designed to actively work on the customer’s behalf.

AI is about to change that assumption entirely. And the most powerful version of this change is one the customer barely notices.

Imagine a transactional account that does not wait for the monthly statement to reveal a pattern. It observes every transaction as it happens and responds. It notices that a standing order will overdraw the account in four days and automatically sweeps in funds from a linked savings pot. It detects that a subscription has increased by fifteen euros without warning and surfaces that as an alert before the payment clears. It identifies lifestyle creep; the gradual accumulation of commitments that erodes a customer’s financial position month by month and flags it proactively, suggesting cancellations or budget adjustments before the damage compounds. And when the bank’s supervisory authority asks how many vulnerable customers it has, the bank will have that number immediately to hand and also be able to tell the regulator the remedial actions already being taken.

A financial institution that can see a customer’s full financial behaviour can configure products that are genuinely individual, not just broad segments but genuine hyper-personalisation.

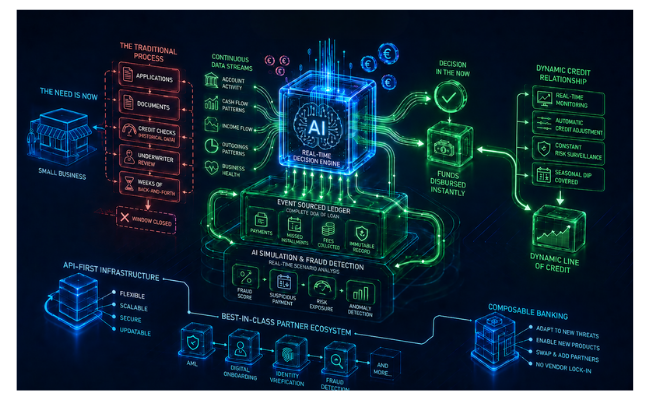

This is the banking nerve centre: doing the work without demanding the customer’s attention. But none of it is possible on a legacy core banking platform that processes in batches and cannot expose real-time data to the systems that need it. Core banking software built for a previous era was designed around human decision cycles, daily reconciliation, monthly statements, quarterly reviews. Banking automation software that operates at AI speed requires a completely different foundation.

CQRS architecture is what makes this possible at scale. By separating read operations, e.g. balance queries, from write operations such as payment transactions, banks can layer complex AI features, delivering real-time carbon tracking, automated merchant categorisation, subscription fatigue analysis directly onto the transaction feed without affecting the speed of the payment itself. Insights appear in the customer’s app the second a card is tapped, not in a report generated overnight or at the end of the month. All this delivers value to their clients and profits and resilience to the business.

API-first infrastructure deepens this further. A transactional account platform drawing on open banking feeds and connected partner data creates a continuously updated picture of the customer’s full financial life: income timing, spending categories, savings habits, life events. all visible, all actionable. This is composable banking in practice: a core account product enriched by best-of-breed partners, integrated through open APIs, and reconfigured as the customer’s needs evolve. A financial institution that can see this whole picture can design and deliver products that are genuinely individual: the fee threshold that reflects this customer’s usage, the overdraft buffer sized to their actual pattern, the notification timing matched to when they are likely to act.

Product configurability is what turns that insight into action. When account parameters. transaction rules, interest tiers, fee triggers, and sweep thresholds are configuration decisions rather than code changes that require regression testing, banks can adjust as they learn without waiting for an engineering cycle.

The transactional account has always been the closest thing banking has to a daily relationship with a customer. With AI paying attention to every event in real time, that relationship finally has the potential to be genuinely valuable: not just a ledger, but a financial partner working quietly, continuously, in the customer’s interest.