AI in Banking: The Revolution Has Begun

The question is no longer whether AI will transform financial services. It already is. The real question, the one that separates the institutions that will lead from those that will follow, is whether their infrastructure can support what comes next.

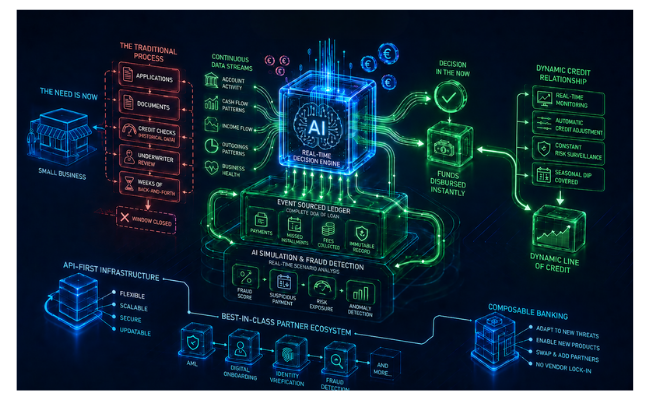

For decades, financial services ran on a model built around human decision-making: a customer applies, a human reviews, a system records. AI is inverting that logic entirely. The machine now analyses, decides, and acts, often in milliseconds, at a scale no human team could match.

We have already seen the first AI-initiated live payment executed within a regulated European banking system. AI agents are managing cash flow for small businesses, automatically renegotiating supplier terms and drawing on credit lines without a human touching the keyboard. Fraud is being caught in real time, not flagged for review, but blocked outright, before the transaction completes. This is not a future scenario. It is happening now.

AI is only as good as the data it consumes. If your data is trapped in a legacy batch-processing system, your AI is operating on yesterday’s news.

The constraint is infrastructure. Most banks are running core banking software that was never designed for a world where software has agency. Legacy core banking platforms process in batches, expose data through retrofitted APIs, and treat every change as an engineering project. Banking automation software cannot operate intelligently on top of a system that delivers data hours after the fact.

The architectural answer lies in how data is handled at the core. Event Sourcing means every financial transaction is recorded as an immutable event, not just the final state, but every step that led there. This creates a granular, real-time audit trail of customer behaviour. Command Query Responsibility Segregation (CQRS) then separates the read operations that AI uses to analyse, from the write operations that process transactions, so intelligence and execution never interfere with each other.

API-first infrastructure completes the picture. When a core banking platform exposes and consumes data through well-designed APIs, it becomes a hub, connecting credit bureaux, identity verification providers, financial wellness tools, and the next generation of fintech partners. This is the foundation of composable banking: assembling best-of-breed capabilities around a clean, open core rather than depending on a single monolithic vendor. The richer the data flowing through the system, the better financial institutions can understand their customers, not as account numbers, but as individuals with specific financial lives, patterns, goals, and needs. That understanding is the foundation of hyper-personalisation and profitable growth for the institution.

Product configurability is the mechanism that turns insight into action. When product parameters, interest tiers, fee structures, transaction limits, eligibility rules, are configuration decisions rather than code changes, a bank can move from understanding a customer segment to serving it without an engineering cycle standing in the way.

SaaScada built its core banking software on exactly these principles: to move the ledger from being a system of record to a system of intelligence, real-time, event-driven, and built for an era where AI does the analysis, the decisions, and the action.

Over the next three articles, we explore what this means in practice for savings accounts, transactional accounts, and lending. In each case, the technology delivering agentic AI in banking is advancing fast. The constraint, and the opportunity, lies in whether the infrastructure underneath can keep up.