Why Flexibility Wins: The Case for a Nimble Partner Ecosystem Over Bank-in-a-Box

All-in-one solutions promise simplicity. But for financial institutions serious about differentiation, growth, and long-term resilience, assembling a best-in-class partner ecosystem is the smarter, and safer, path forward.

All-in-one platforms reduce vendor complexity. They also reduce your ability to differentiate in your market. As AI-native partners, embedded finance providers, and specialist fintechs repeatedly redefine what best-in-class looks like across every banking function, the institutions with open, composable infrastructure are moving faster, integrating new capabilities in weeks, not quarters. The partner ecosystem model isn’t a workaround. For banks serious about long-term competitiveness, it’s the strategic foundation.

The promise of a Bank-in-a-Box, using your own licence, or even leveraging the licence of Banking-as-a-Service (BaaS), is seductive: one vendor, one contract, one full-stack banking platform to handle everything from current accounts to lending, compliance to reporting. For a leadership team under pressure to modernise quickly, it can look like the lowest-risk path. But organisations that have lived through the reality tell a different story, one of vendor lock-in, constrained product development, and a slow, expensive crawl towards the kind of innovation that nimbler competitors are already delivering.

The alternative, building a flexible partner ecosystem around a modern core banking platform, is not the riskier option. It is, in fact, the more measured and future-proof approach. Here’s why.

Differentiation Requires the Freedom to Choose

At the heart of every strategic technology decision is a deceptively simple question: where do you want to differentiate? Target audience, size, product offering? The answer shapes everything, including whether a bundled, all-in-one solution will serve you well or hold you back.

Consider the distinction between two types of financial institutions. The first is a bank whose competitive advantage lies in its community relationship, in reaching an underserved segment that isn’t getting access to financial services, not because the products aren’t right, but because the communication and distribution channels have failed them. For this institution, a Bank-in-a-Box arrangement or a ready-packaged end-to-end solution may be entirely appropriate at launch. The product is not the differentiator. The relationship is. Once established, after gaining insights and identifying how better to individually serve tranches of their customers, the bank might then decide for a more nimble core banking solution.

Now consider a second institution, one built specifically to challenge the way a particular financial product, say mortgages, works. For this organisation, an off-the-shelf solution is likely to be a ceiling, not a foundation. Product innovation is central to their proposition, so a bundled lending software may struggle to deliver the specific capabilities they need. It is inherently a slightly more one-size-fits-all solution.

This isn’t a criticism of Bank-in-a-Box providers, it’s an honest acknowledgement that bundled solutions are designed to serve those who are delivering basic services, not to enable exceptional, innovative ones. For institutions whose edge lies in how they serve customers, rather than who they serve, that distinction is critical. If you want to settle for tooling for perceived ease in the first instance, then Bank-in-a-Box can be a tempting, but you must also look at how it will impact growth. This choice will likely hobble innovation in the future as you look to innovate and scale.

Flexibility Is a Regulatory Asset, Not Just a Commercial One

The regulatory environment for financial services is in constant motion. Institutions that have locked themselves into a single vendor’s interpretation of compliance requirements can find themselves exposed when regulations shift, or when their vendor is slow to adapt, for example in response to regional regulatory variations. A partner ecosystem approach, by contrast, allows institutions to work with specialists, compliance, KYC, AML, reporting, who are entirely focused on maintaining best-in-class solutions within their domain.

The Ecosystem Model Offers Control

Critics of the partner ecosystem approach often argue that it introduces complexity, multiple vendors, multiple contracts, multiple integration points. There is truth in this. Yet the alternative is not simplicity. It is the illusion of simplicity: a single surface beneath which a bank has ceded control of its technology roadmap to a vendor whose priorities may not always align with its own.

Technology changes. Business processes evolve. The skills and thinking within an institution shift. With a composable banking mindset a selectively chosen partner ecosystem accommodates all of this, allowing each layer to be upgraded, replaced, or enhanced whenever appropriate, without disrupting the whole.

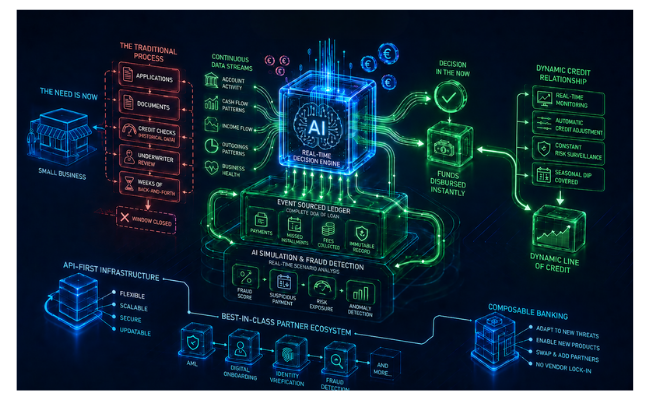

Consider loan servicing software as an example. A Bank-in-a-Box bundles this capability into its platform, locking you into a single vendor’s roadmap. A composable banking approach lets you select a cost effective best-in-class loan servicing specialist and integrate it cleanly via API-first infrastructure, giving you the freedom to swap, upgrade, or extend that capability as your needs evolve.

A Bank-in-a-Box, by contrast, is a wager that one vendor has anticipated every product you will ever want to offer, every market you will ever want to enter, and every regulatory requirement you will ever face. That is not a wager institutional leaders with foresight would be comfortable placing, because it is not one they should have to. Given the changing nature of financial services and innovative financial technology, the ability to choose best-of-breed tooling and services is important. Your needs will change, so agility is key.

The AI Imperative: Why Your Ecosystem Needs AI-Native Partners

If the argument for a flexible partner ecosystem was already compelling, the rapid emergence of artificial intelligence has made it urgent. AI is arriving as a new category of specialist partner, purpose-built to deliver capabilities that no all-in-one vendor has yet mastered, and that most never will because their full-stack offering is often the result of acquisitions that work clumsily with one another. For financial institutions serious about staying competitive, the ability to plug AI-native partners into their ecosystem is no longer a nice-to-have. It is becoming a core requirement of the technology strategy.

The use cases are already well established in forward-thinking institutions: AI-driven credit decisioning that assesses risk beyond traditional scoring models; real-time fraud detection that adapts to emerging patterns faster than any rules engine; hyper-personalised customer engagement that responds to individual behaviour rather than demographic segments; and AI-assisted compliance monitoring that reduces manual overhead while improving accuracy. In each of these domains, there are focused specialists building and refining models against a single problem, and improving at a pace that a bundled solution simply cannot match.

This is precisely where the Bank-in-a-Box model reveals its deepest limitation. A closed platform controls what data is exposed, how it is structured, and what third-party integrations are permitted. AI, by contrast, demands access to clean, granular, real-time data. It requires an API-first infrastructure that can pass the right signals to the right applications at the right moment. Institutions locked into a legacy data model, or a vendor’s proprietary data layer, will find themselves unable to take full advantage of the AI partners entering the market. The ecosystem approach, built on an open, event-driven core banking platform, removes that ceiling entirely.

The most important currency in a Financial Institution has long been data. For an institution to succeed, its relationship with its customers must go beyond the transactional. Data is essential to drive AI and enable institutions to deliver the personalisation that will be expected from tomorrow’s banking by business, retail and institutional customers.

The institutions that will lead in the next five years and beyond are not those that waited for their existing vendor to bolt AI onto an existing product. They are those who built the architectural foundations to work with best-in-class AI partners as they mature, and that gave themselves the freedom to swap, upgrade, or add new capabilities as the landscape evolves. That freedom is not something a Bank-in-a-Box can offer. But it is exactly what a well-designed partner ecosystem, underpinned by modern core banking software and open API-first infrastructure, is built to provide.

Build for the Bank You Are Becoming

The question every financial institution must ask is not simply “what do we need today?” but “what will we need in three, five, or ten years?” The bank that is growing, evolving, and competing in an increasingly dynamic market needs a technology foundation that can grow, evolve, and adapt alongside it.

The flexible partner ecosystem, built around a cloud-native core banking software foundation, assembled from best-in-class specialists, including dedicated digital lending platform providers, specialist loan servicing software vendors, and implemented progressively through a coexistence model, is not a compromise between innovation and stability. It is the architecture that enables both. Rooted in composable banking principles and connected via API-first infrastructure, it allows institutions to innovate at the edge without risk to the centre, migrate without disruption, and scale without prohibitive cost.

The Bank-in-a-Box will always offer a fast start. But in a world where financial services are being reshaped by technology, regulation, and customer expectation in equal measure, the institutions that will thrive are those that choose not to limit their future on day one.